On April 30, 2026, President Donald Trump issued an executive order establishing TrumpIRA.gov, a new federal platform designed to make retirement saving simpler and more accessible for American workers who lack employer-sponsored plans. This move targets the large group of employees—often in small businesses, gig work, or part-time roles—who currently have limited options for building long-term wealth.

Rather than creating an entirely new retirement account category, the initiative focuses on removing barriers to existing Individual Retirement Accounts (IRAs) while expanding the Saver’s Match program. It emphasizes practical, disciplined saving in line with proven strategies from investing legends like Jack Bogle’s emphasis on low-cost index funds, Warren Buffett’s patient approach to compounding, and Benjamin Graham’s focus on avoiding unnecessary risks.

Quick Navigation

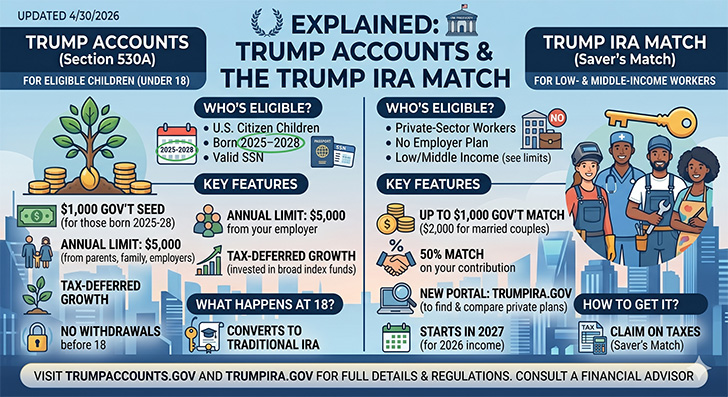

Who Can Benefit from Trump IRA Accounts?

The primary audience includes the estimated 40-80% of workers (depending on full-time or part-time status) whose employers do not offer 401(k)s or similar plans.

Starting in 2027, qualifying lower-income individuals can receive a government match of up to $1,000 per year through the Saver’s Match. This credit generally targets singles earning below roughly $35,500 and married couples filing jointly under about $71,000 (thresholds are subject to inflation adjustments). The match provides up to 50% of your contributions, deposited straight into your chosen retirement account.

The website will serve as a user-friendly marketplace where anyone can browse, compare, and open private-sector IRA options based on fees, investment choices, and minimum requirements. This setup aims to guide people toward transparent, cost-effective plans instead of high-commission products.

How TrumpIRA.gov Differs from Traditional Retirement Accounts

TrumpIRA.gov does not replace or reinvent core retirement vehicles—it makes them easier to access:

- Compared to Employer 401(k) Plans: No need for employer involvement or matching contributions (though some linked plans might still offer them). Contribution limits remain the standard IRA amounts (currently around $7,000 for those under 50, with catch-up provisions for older savers—always confirm latest IRS figures). Setup happens independently through the platform.

- Compared to Regular IRAs: The big upgrade is convenience. The site lowers the entry hurdles for self-employed individuals, freelancers, and others by providing clear comparisons and direct pathways to enrollment. It also layers on the Saver’s Match incentive for eligible households.

- Separate from Child “Trump Accounts”: Keep in mind that the adult-focused TrumpIRA.gov is distinct from the child-oriented Trump Accounts program (created under the 2025 legislation). Those custodial accounts provide a $1,000 federal seed deposit for qualifying births and allow family contributions, with assets converting to standard IRAs at age 18. The April 30 announcement centers on working adults.

Tax rules stay consistent with familiar IRA options: Traditional IRAs may offer upfront tax deductions (subject to income limits), while Roth IRAs provide tax-free growth and qualified withdrawals. Early withdrawals before age 59½ typically incur penalties to encourage long-term commitment.

Timeline, Features, and Investment Guidance

The platform is currently in development, with full integration of the Saver’s Match expected for the 2027 tax year. Users will be able to select from approved private providers, ideally favoring low-expense-ratio index funds or broad-market ETFs that track the overall economy.

This approach aligns perfectly with time-tested wisdom:

- Buy and hold diversified portfolios rather than chasing hot stocks.

- Minimize fees so more of your money stays invested and compounds over decades.

- Focus on broad U.S. market exposure, as supported by efficient market principles from thinkers like Burton Malkiel and Paul Samuelson.

Future enhancements may include automatic enrollment tools or opportunities for private contributions to boost accounts further.

Why This Initiative Matters for Long-Term Financial Health

Retirement readiness remains a pressing issue for many families. By connecting underserved workers to simple, low-cost saving tools, TrumpIRA.gov addresses a meaningful gap without adding unnecessary complexity to the system.

From a stewardship perspective, consistent saving reflects wise management of resources. Even small, regular contributions—especially when boosted by a government match—can grow substantially through the power of compounding. Pair this with debt reduction and emergency savings for a solid foundation.

Practical Steps to Take Advantage of TrumpIRA.gov

- Assess your situation: Determine whether your employer offers a retirement plan and review your current savings rate.

- Watch for the launch: Visit TrumpIRA.gov when it goes live for plan comparisons and enrollment instructions.

- Maximize the match: If your income qualifies, prioritize contributions that unlock the full $1,000 annual Saver’s Match.

- Choose wisely: Select providers with rock-bottom fees and straightforward index fund options. Avoid complex or high-cost investments that erode returns.

- Seek professional input: Consult a fee-only financial advisor or tax professional to ensure the strategy fits your full financial picture, including other accounts like HSAs or 529 plans.

This initiative represents a pragmatic step toward broader retirement security. It complements rather than competes with existing tools, encouraging more Americans to participate in the market steadily over time instead of trying to time it. By focusing on discipline, low costs, and patience, families can build meaningful wealth across generations.

This information is for educational purposes only. Program details, income thresholds, and tax rules may evolve—consult official IRS guidance or a qualified advisor for personalized advice.

Share Your Thoughts: